How to Buy a Home with BAH in the Fort Riley Area: Making the Numbers Work

If you're stationed at Fort Riley and receiving BAH, you're already sitting on one of the most powerful home-buying tools available — a tax-free monthly housing allowance that doesn't disappear whether you rent or own. The question isn't whether BAH can help you buy. It's whether you've actually run the numbers to see what it buys you here.

This post does exactly that. Real 2026 rates. Real mortgage math. Real examples based on what's actually available in the Fort Riley housing market.

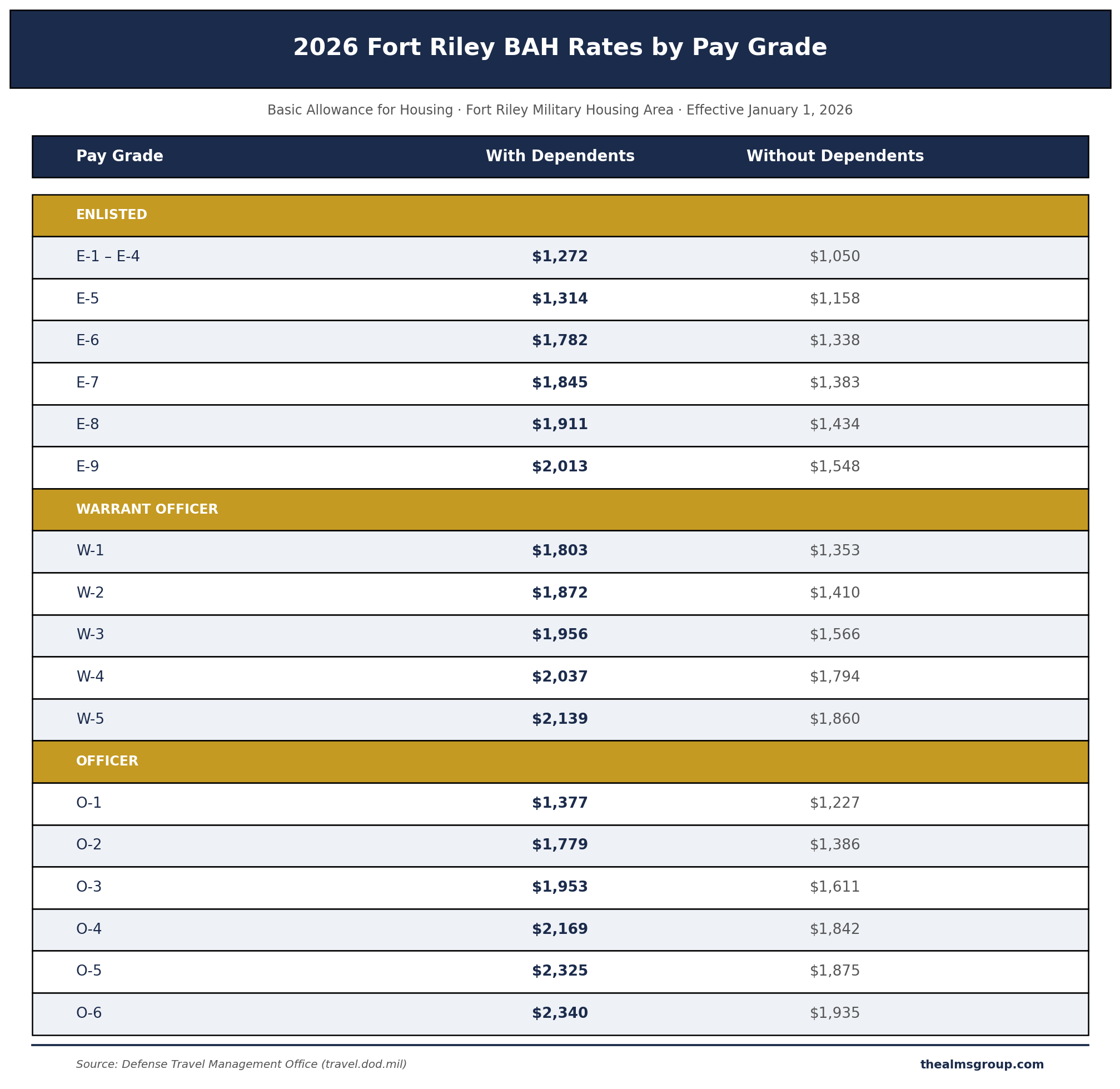

Your 2026 BAH at Fort Riley

BAH is calculated based on your pay grade, dependency status, and duty station zip code. Here's what the full table looks like for the Fort Riley Military Housing Area in 2026:

One thing worth noting: Fort Riley's BAH increased 6.6% over 2025. That's meaningful — and it's one reason the math of buying here has gotten more favorable in recent years.

Translating BAH Into Buying Power

The key question is: what does your BAH actually cover when it comes to a mortgage payment?

A VA loan changes the equation significantly. Because VA loans require no down payment and no private mortgage insurance (PMI), your monthly payment is lower than it would be on a conventional loan at the same price. That gap — what you'd normally pay in PMI alone — is often $100–$200/month that stays in your pocket.

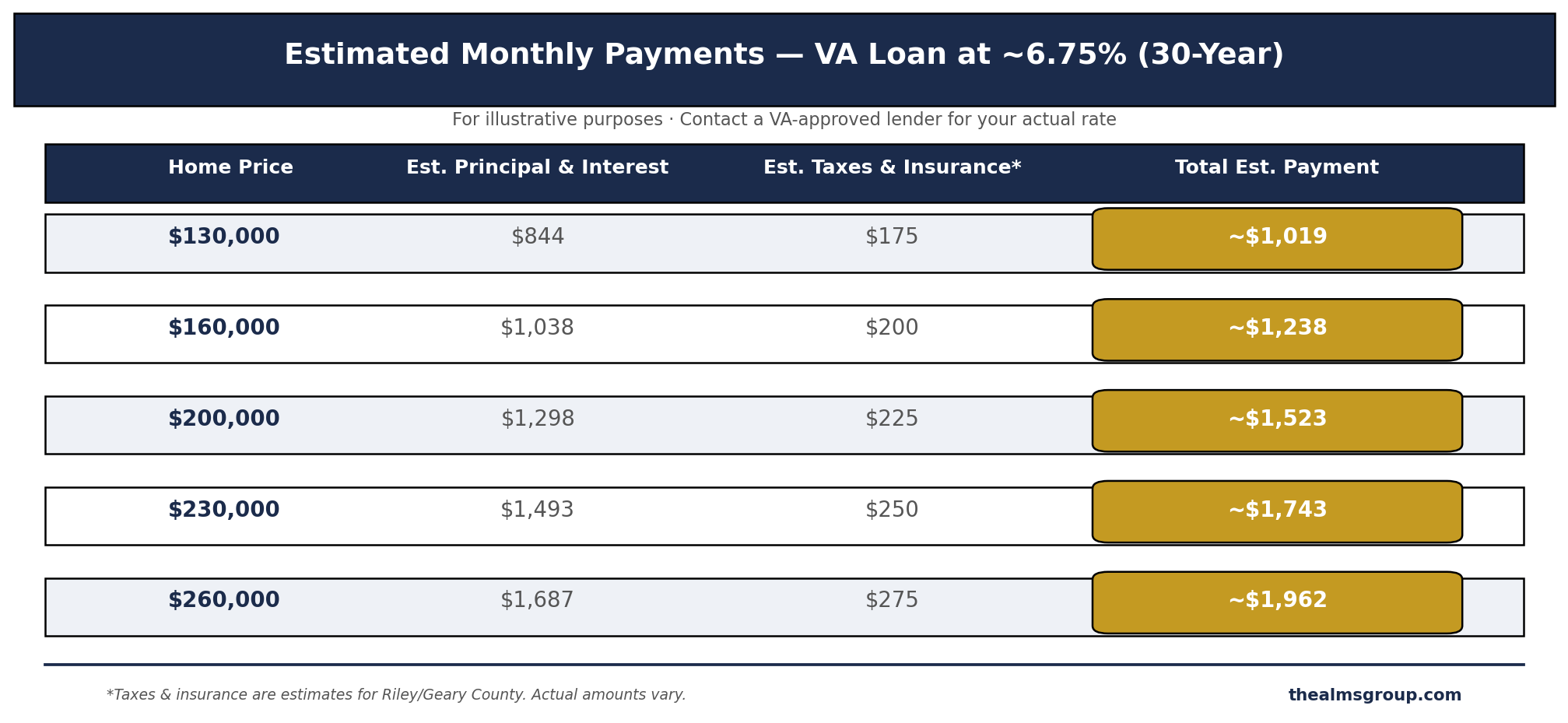

To give you a working example, here's what monthly payments look like at different price points using a 30-year VA loan at approximately 6.75% interest (rates vary — check with a VA-approved lender for your actual rate):

Taxes and insurance are estimates based on typical Riley/Geary County rates. Your actual amounts will vary.

What the Numbers Look Like by Rank

E-5 with Dependents — $1,314/month BAH

At $1,314/month, an E-5 family has solid buying power in Junction City, where home prices average around $109,000–$130,000. A $130,000 home with a VA loan runs approximately $1,019/month in total payment — meaning BAH covers it entirely, with roughly $295/month left over.

In Manhattan, where the median home price is closer to $250,000, an E-5's BAH won't cover a full mortgage payment. The gap would be approximately $200–$400/month depending on the home. That's manageable for many families, but it means buying in Manhattan requires a clear-eyed budget.

Bottom line for E-5: Junction City likely pencils out to BAH-neutral or better. Manhattan requires some out-of-pocket contribution but may still be worth it depending on schools and lifestyle priorities.

E-6 with Dependents — $1,782/month BAH

This is where the math starts to get genuinely interesting. At $1,782/month, an E-6 family has meaningful buying power in both markets.

In Junction City, a $130,000–$160,000 home runs roughly $1,019–$1,238/month all-in. That leaves $544–$763/month of BAH unspent — money that, if put toward principal or savings, can accelerate equity significantly over a 3-year tour.

In Manhattan, a $230,000 home runs approximately $1,743/month. An E-6's BAH of $1,782 covers it — essentially dollar-for-dollar. At that price point, you're in solid inventory in Manhattan, particularly in established neighborhoods like Westloop or south Manhattan.

Bottom line for E-6: Both markets work. In Junction City, BAH exceeds the payment. In Manhattan, the payment is roughly BAH-neutral at the right price point.

O-3 with Dependents — $1,953/month BAH

An O-3 family has the most flexibility of the common pay grades at Fort Riley. At $1,953/month, BAH is sufficient to cover a $250,000–$260,000 home in Manhattan — which is right at the median and puts you in good inventory across the city.

A $260,000 home runs approximately $1,962/month all-in. That's nearly a dollar-for-dollar BAH match, and it opens up newer construction in areas like the northern part of Manhattan or closer to K-State.

Bottom line for O-3: Manhattan's median market is essentially designed around your BAH. You have the most room to choose between location, school district proximity, and home size without budget stress.

When BAH Exceeds Your Mortgage Payment

One scenario that catches people off guard: what happens when your BAH is more than your mortgage payment?

This is a real possibility — particularly for E-6 and above in Junction City, or for any service member buying well below their BAH ceiling. Because BAH is paid to you directly (it's not sent to a landlord or lender), any amount left after your housing costs is yours to use however you choose. There's no requirement to spend it all on housing.

For homeowners, that surplus can go toward accelerated mortgage paydown, an emergency fund, home improvements, or simply more financial breathing room. Over a 3-year tour, even $200–$300/month of surplus adds up to $7,200–$10,800.

What to Watch Out For

The numbers above give you a solid framework, but a few variables can move the math:

Interest rates. VA loan rates fluctuate. The examples above use approximately 6.75% — your actual rate could be higher or lower. Get pre-approved before you start shopping so you know exactly what your payment looks like.

Property taxes and HOA fees. Riley and Geary County property taxes are relatively low by national standards, but HOA fees (common in some Manhattan developments) can add $50–$200/month to your cost. Factor these in.

BAH doesn't cover every homeownership cost. Maintenance, utilities, and repairs aren't covered by BAH. Budget an additional 1–2% of home value per year for upkeep.

BAH is tied to your duty station, not where you live. If you live in Manhattan but are stationed at Fort Riley, you receive Fort Riley BAH — not a higher rate for living farther away.

Running Your Own Numbers

The best way to get a precise picture before making any decisions:

Confirm your BAH rate at travel.dod.mil using Fort Riley zip code 66442.

Get pre-approved for a VA loan with a lender who works regularly with military buyers — they'll give you an actual interest rate and payment estimate based on your credit and income.

Talk to a local agent who knows both the Manhattan and Junction City markets and can show you what's available at your price point.

The Alms Group works regularly with service members and families relocating to the Fort Riley area. If you want a straightforward conversation about what your BAH will realistically get you — in either market — we're happy to run through the numbers with you.

Contact our team to get started.

BAH rates are effective January 1, 2026, and are subject to change annually. Mortgage payment estimates are for illustrative purposes only and do not constitute a loan offer. Contact a VA-approved lender for your actual rate and payment.